The Nixon Shock

Few days in modern economic history are remembered as a day of infamy like August 15, 1971, when President Richard Nixon suspended U.S. dollar’s convertibility to gold. The “Nixon Shock” permanently and fundamentally transformed U.S.’s economy and governance, its impact reshaped international trade and geopolitics.

Taking place during the Pluto trine (when transiting Pluto formed a 120° angle to the U.S. Pluto), this series of events played out along the path of political expediency and betrayal of principles, which were followed by pernicious effects. The result was the corruption of core values (Pluto in 2nd house): currency devaluation, economic recession, a tectonic shift of socioeconomic landscape, and the government’s increased control over personal freedom and prosperity – all signatures of U.S. Pluto transits.

The trine between two planets indicates both energies working in sync and in harmony. The influences materialize swiftly. Due to the lack of conflict, the natives can be careless and unaware. In the case of U.S. Pluto, the trine with transiting Pluto means the powerful, corruptive forces –both within and without—are working as one, unobstructed. What we observed was the compromise of core beliefs, broken promises, deceptions, and secrecy.

Policies made during U.S. Pluto transits often corresponded with the destruction of status quo and the expansion of federal government. The quick-and-dirty solution frequently leads to unintended consequences that work the opposite of the original intention, since Pluto’s pattern is also to ensnare and complicate. The impact of these policies does not fully materialize until years, even decades later. This episode is a cautionary tale of a politicized economy and its aftermath.

Consumer Price Index: Food in U.S. City Average (Green)

Consumer Price Index: Energy in U.S. City Average (Red)

Median Sales Price of House in the U.S. (Purple)

Median family income (Gold)

1960 – 2022. Price in August (Q3) 1971 is indexed at 100

Transit Pluto trine U.S. Pluto (120-degree angle)

Effective periods:

November 4, 1969 – February 26, 1970

September 2, 1970 – October 27, 1970

March 12, 1971 – August 26, 1971

Exact dates: September 29, 1970; April 20, 1971; July 24, 1971

Themes:

- Compromise of principle for political expediency

- Financial crisis, inflation, and currency devaluation

- Plutonomy (Wealth redistribution, disparity, and concentration)

- Plutocracy (Expansion of government control. Government by the wealthy, of the wealthy, and for the wealthy.)

- Trade wars and currency wars

THE BRETTON WOODS SYSTEM

In July 1944, near the end of World War II, delegates from 44 nations gathered at the Bretton Woods Conference to rebuild the international monetary system. United States dominated the post-war economy and its dollar emerged as the world’s reserve currency. The U.S. government agreed to back every dollar overseas with its gold reserve at $35 per ounce, and all other countries pegged their currencies to the dollar.

The Bretton Woods system became functional in 1958. Since U.S. owned over half of the world’s gold reserve, the system was stable for a time. Foreign countries continued to acquire dollars and spend on American industrial exports, and their U.S. dollars were saved in interest-bearing accounts rather than converted to gold (Lowenstein 2011).

THE LONDON GOLD POOL

In order to provide dollars for international trade, U.S. ran a persistent balance of payment deficit (expenditure exceeding income) and redeemed overseas dollars in gold upon request. In 1961, the amount of outstanding dollar claims began to exceed the U.S. government’s gold reserve. The London Gold Pool was established to shoulder the burden of gold outflow with member nations and defend the $35 gold price.

The stabilization mechanism was not to last. The Federal Reserve shifted to an inflationary policy in 1965, violating the rules of the Bretton Woods System (Bordo, Monnet, and Naef 2017). In the same year, French president Charles De Gaulle led the charge to repatriate gold and subsequently withdrew from the London Gold Pool. Other countries followed suit and the gold run accelerated.

Unfazed, the U.S. government carried on its “benign neglect” policy, running ever-larger balance of payments deficits and increased spending on Great Society program and the Vietnam war. The Johnson administration (1963-1969) doubled the national deficit and flooded the world with dollars.

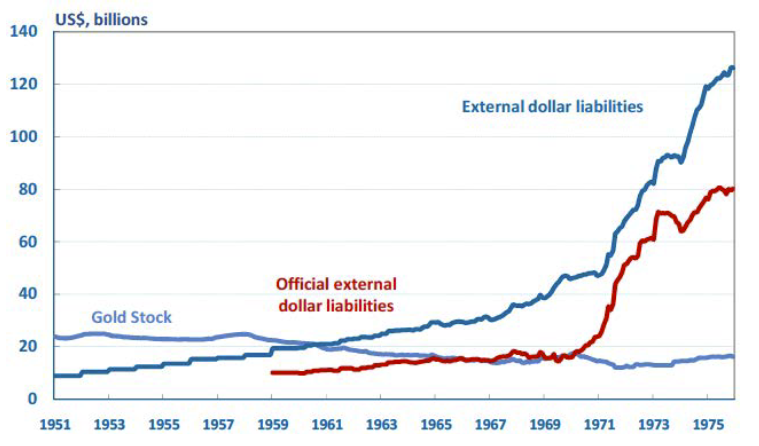

As the U.S. dollar became further overvalued and oversupplied, foreign central banks and traders accelerated their dollar-to-gold conversion. In 1966, foreign central banks and governments held over 14 billion U.S. dollars. The United States had $13.2 billion in its gold reserve, only $3.2 billion of which was available to cover foreign dollar holdings.

On March 14, 1968, the United States requested the London gold markets to halt trading amidst overwhelming demand; the two-week closure spelled the official collapse of the London Gold Pool. On March 18, the congress voted to eliminate the gold reserve requirement for Federal Reserve Notes –namely, the U. S. Dollar. The measure exacerbated the devaluation and damaged the U.S.’s credibility. (Bordo 2018)

A two-tiered gold system emerged in effort to shore up the U. S. dollar and contain gold’s surging price. Foreign central-banks pledged to stop trading gold on the open market and reaffirmed the $35 price among central banks. Gold price in the open market was left to float freely. Incidentally, American citizens had been barred from owning monetary gold since 1933. The U.S. Supreme Court ruled the gold confiscation was constitutional during U.S. Pluto and transiting Pluto opposition (forming a 180-degree angle) in 1935.

THE DOLLAR CRISIS OF 1971

What’s our immediate problem? We are meeting here today because we are in trouble overseas. The British came in today to ask us to cover $3 billion, all their dollar reserves. Anyone can topple us – anytime they want – we have left ourselves completely exposed.

—John Connally, Secretary of the Treasury (1971-1972), August 1971

The fiscal and monetary tightening in 1968 brought some relief to the gold outflow; it also caused the recession in 1970. Despite inflation nearing a two-decade high, Nixon was more worried about persistent high unemployment rates, fearing it would threaten his re-election victory. He relentlessly harassed and pressured Burns –through whisper campaigns, blackmailing and mixed messages –to accelerate money supply “vigorously and aggressively”. Starting in early 1971, Burns forwent his cautious stance and repeatedly slashed the Fed discount rate. Inflation and the run on the dollar resumed. In June 1971, gold in the open market rose above $40 per ounce.

In early August of 1971, United States lost $850 million in gold reserves in just one week. The French had called in over $1 billion in reserves in the a few weeks prior (after an $191 million purchase); the Germans and the Dutch were looking to call in some $200 – 250 million more. (Ohlmacher 2009)

The last draw came on August 12, when the British ambassador appeared before the United States Treasury and asked that $3 billion be converted into gold. That amounted to one quarter of the remaining U. S. gold reserves.

With the run on the dollar at an all-time high and Nixon administration unwilling to tighten, the Bretton Woods framework reached a breaking point. Nixon had wanted to hold off a decision until after the 1972 election, but was advised that doing so would risk hemorrhaging billions more from the gold reserves. To put an immediate stop to market speculation, Nixon’s advisors impressed upon him that the announcement must be made before the markets’ open on the next Monday, which meant broadcasting during the Sunday prime time.

SECRET CAMP DAVID MEETING

On the afternoon of Friday, August 13, 1971, President Nixon holed up with fifteen advisers and staff members at Camp David to confront the economic crisis. The course of action was set: all that was needed was a united front within the administration. Nixon was preoccupied with the short-term economic outcomes and how it would impact of his re-election in 1972 (Ohlmacher 2009); more time was spent discussing the timing and the presentation of the speech than how the economic program would work (Yergin and Stanislaw 1997). Despite of the policy’s enormous impact on international relations and global trade, no foreign policy advisors were invited. Federal Reserve chair Arthur Burns vehemently opposed the closing of the gold window, but he was marginalized and overruled.

Secretary of Treasury John Connally played to the president’s insecurity and advocated dramatic display of leadership. Having infamously said “foreigners are out to screw us … our job is to screw them first,” Connally convinced the president to bypass the Congress and plan in secret ahead of the European finance ministers’ meeting, which would release a joint statement on the United States’ role in the international financial crisis (Ohlmacher 2009).

We can stop convertibility very easily – by just saying so…The next thing is that you probably ought to float this exchange rate with the other currencies of the world. …We have a floating currency… We can take these steps without revaluing gold.

—John Connally, Secretary of the Treasury, August 1971 (Ohlmacher 2009)

Connally assured Nixon that he did not have to be the president who devalued the dollar, and advised him to conflate the closing of the gold window with a domestic policy package: “Whatever we do in the international field – it seems to me – ought to be coupled with action on the domestic front so that they tend to shield each other”. “Posture it as being competitive,” such action would have “no political downsides. At all. And a great deal of upsides”. (Ohlmacher 2009)

THE NIXON SHOCK (& LIES)

On the evening of August 15, 1971 president Nixon delivered a live, prime-time speech to outline his sweeping economic reform. In a broad stroke, Nixon proposed a 10 percent tax credit for business investment, repeal of the 7-percent excise on automobiles, and speeding up income tax exemption. He also ordered a cut in Federal spending and foreign aid, pay freeze, and downsizing government personnel.

By executive order, Nixon imposed a 90-day wage and price control to counteract inflation expectations. As his dramatic announcement seemingly drew to a close, Nixon segued into blaming international currency traders for unemployment and inflation, arguing for a strong dollar, trade competitiveness, decoupling from gold, and monetary stability in the same breath:

The third indispensable element in building the new prosperity is closely related to creating new jobs and halting inflation. We must protect the position of the American dollar as a pillar of monetary stability around the world.

In the past 7 years, there has been an average of one international monetary crisis every year. Now who gains from these crises? Not the workingman; not the investor; not the real producers of wealth. The gainers are the international money speculators. Because they thrive on crises, they help to create them.

In recent weeks, the speculators have been waging an all-out war on the American dollar. The strength of a nation’s currency is based on the strength of that nation’s economy, and the American economy is by far the strongest in the world. Accordingly, I have directed the Secretary of the Treasury to take the action necessary to defend the dollar against the speculators. I have directed Secretary Connally to suspend temporarily the convertibility of the dollar into gold or other reserve assets, except in amounts and conditions determined to be in the interest of monetary stability and in the best interest of the United States.

Now, what is this action which is very technical? What does it mean for you? Let me lay to rest the bugaboo of what is called devaluation. If you want to buy a foreign car or take a trip abroad, market conditions may cause your dollar to buy slightly less. But if you are among the overwhelming majority of Americans who buy American-made products in America, your dollar will be worth just as much tomorrow as it is today….

I am determined that the American dollar must never again be a hostage in the hands of international speculators.

I am taking one further step to protect the dollar, to improve our balance of payments, and to increase jobs for Americans. As a temporary measure, I am today imposing an additional tax of 10 percent on goods imported into the United States. …

As a result of these actions, the product of American labor will be more competitive, and the unfair edge that some of our foreign competition has will be removed. This is a major reason why our trade balance has eroded over the past 15 years.

–President Richard Nixon, August 15, 1971

With this announcement, U.S. unilaterally suspend the dollar’s convertibility into gold, effectively dissolved its international obligations and ended the Bretton Wood system. Nixon blamed “international speculators” for U.S. losing competitiveness and imposed a 10% tariff on all imported goods until a new international monetary agreement was made.

President Nixon has moved with startling decisiveness to stabilize the dollar and spur economic growth. … (He) has now provided the leadership which is even more essential than any specific proposal for turning the economy around and starting it back on the road to full employment, price stability and competitiveness in an open world market.

–The New York Times, August 16, 1971

The new policy was well-received by the media as well as Wall Street, with the S&P 500 booking the largest one-day gain of the year.

POLITICAL EXPEDIENCY

… between now and the election in November [1972], there must be one paramount consideration. And that paramount consideration is not the responsibility of the U.S. in the world, it isn’t outgoing policy, it isn’t the fact that in foreign [policy] we’ve done this, that, or the other thing, the main thing is that we have to create the impression that the president of the United States, finally, at long last, after 25 years with blood, sweat and tears, is […] looking after its interests.

–President Richard Nixon, September 11, 1972

Back in 1968, Nixon campaigned on the promise to roll back President Johnson’s liberal agenda and expansionist policies. He presented himself as a free-market proponent in pursuit of gradual money contraction, inflation reduction, full employment, and balanced budgets. (Bordo 2018)

Believing that high unemployment rates had costed him his first presidential bid in 1960, Nixon’s mandate for the incoming Fed Chairman Arthur Burns was “no recessions”. (Bordo 2018) After the mild recession in 1970, Nixon declared “now I am a Keynesian,” abandoning his free-market stance and fiscal discipline. A loose monetary policy not only supported the domestic welfare programs and the Vietnam war, but also supported economic expansion resulting in an upward revision of economic indicators through the election season.

FALSE ENEMIES

Instead of correcting the monetary and fiscal policies, President Nixon successfully convinced the American people that the rest of the world was the problem: The surplus countries were blamed for devaluing their currencies and hurting the dollar’s competitiveness; currency speculators were blamed for the pressure to devalue the dollar. There was an unwillingness to recognize that the key source of the problem: U.S. inflation. (Bordo 2018)

By re-framing policy failure as a triumph and fresh start, Nixon succeeded in playing the role of a strong and decisive leader. He won the re-election in a landslide in 1972.

This is the shabby secret of the welfare statists’ tirades against gold. Deficit spending is simply a scheme for the “hidden” confiscation of wealth. Gold stands in the way of this insidious process. It stands as a protector of property rights. If one grasps this, one has no difficulty in understanding the statists’ antagonism toward the gold standard.

–Alan Greenspan (Federal Reserve Chairman, 1978-2006), 1967

ADDITIONAL READING

- Turmoil in the Second House – The U.S. Pluto Return (2021-2023) Part 1: Astrology

- Turmoil in the Second House – The U.S. Pluto Return (2021-2023) Part 2: Born on the Battlefront

- Turmoil in the Second House – The U.S. Pluto Return (2021-2023) Part 3: History Rhymes (1) |Panic of 1819 and The Missouri Compromise (1819-1821)

- Turmoil in the Second House – The U.S. Pluto Return (2021-2023) Part 3: History Rhymes (3) |Nixon Shock, The Aftermath

©2022 Brave New Real. All rights reserved.