Nixon Shock, The Aftermath

THE COST OF COMPROMISE

SHOCK WAVES FROM WASHINGTON

“…the dollar may be our currency, but it’s your problem…”

–Treasury Secretary John Connolly (Nitchter 2015)

Nixon’s announcement upended the international monetary system (Burns 2010), and caused mayhem in the currency markets. Countries that chose to hold their reserves in U.S. dollars suffered heavy losses and faced widespread economic turmoil. By mid-1973 the U.S. dollar had fallen by 25 percent on average, relative to the major Western currencies (Hammes and Wills 2005). “Shock waves from Washington’s decision to break the link with gold have rippled down the decades. The creation of the euro, the hollowing out of US manufacturing, the arrival of cryptocurrencies and the ability of central banks to print seemingly unlimited quantities of money can all be traced back to August 1971” (Elliott 2021).

I’m really very concerned about the way that things are shaping up politically in every one of these countries. Italy has a recession […] Germany has a recession […] we’re going to Moscow, but Japan is a mess. Western Europe is in a mess. We’ve given up our friends to our enemies.

—National Security Advisor Henry Kissinger, November 16, 1971 (Nichter 2015)

In December 1971, after months of negotiations, the Group of Ten (G-10) industrialized democracies agreed to a new set of fixed exchange rates in the Smithsonian Agreement. U. S. dollar was devalued by 8.5% against gold to $38 per ounce. Europeans revalued their currencies by a similar amount and Japan agreed to revalue Yen by 16.9%.

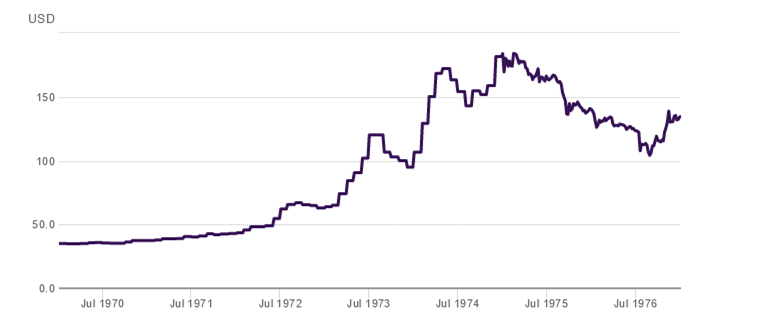

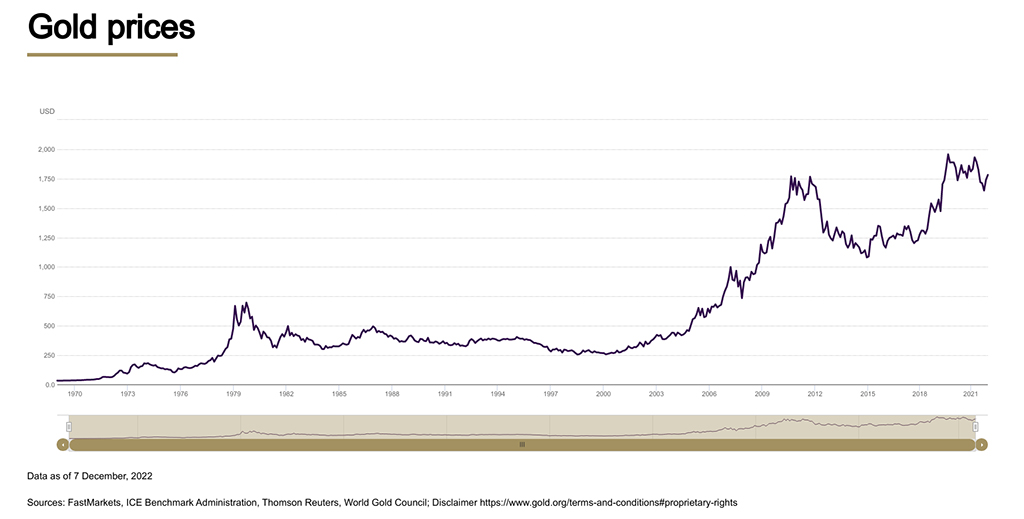

Dubbed “the most significant monetary agreement in the history of the world,” by president Nixon, the agreement was doomed from the start. On February 12, 1973, U. S. dollar devalued by another 10% to $42 per ounce of gold. Speculation against the dollar pushed other major currencies to float against the dollar and rang the death knell for the fixed rate exchange regime. Gold rose to $90 an ounce in mid-1972 and reached $195 by the end of 1974.

Inflation, stagflation, and Price control

Having talked until recently about the evils of wage and price controls, I knew I had opened myself to the charge that I had either betrayed my own principles or concealed my real intentions. Philosophically, however, I was still against wage-price controls, even though I was convinced that the objective reality of the economic situation forced me to impose them. …

What did America reap from its brief fling with economic controls? The August 15, 1971, decision to impose them was politically necessary and immensely popular in the short run. But in the long run I believe that it was wrong. The piper must always be paid, and there was an unquestionably high price for tampering with the orthodox economic mechanisms.

–President Richard Nixon, RN: The Memoirs of Richard Nixon

By all accounts, “Nixon’s economic package was a short-term success. Throughout 1972, the United States enjoyed the largest real growth (5.7 percent) and the lowest rise in consumer prices (3.3 percent) since the Johnson administration. Unemployment declined to 5.1 percent, and the American balance of payments deficit shrunk drastically from $29.8 billion in 1971 to $10.4 billion in 1972” (Nitchter 2015).

The 90-day wage and price control sought to “shield” the American people from the monetary shock and solve the inflation-employment dilemma. Such policy was supposed to allow the administration to maintain a loose fiscal policy without fanning inflation. However, inflation soon reignited after the election. In 1973 another round wage and price freeze failed to curb the inflation and was followed by stagflation.

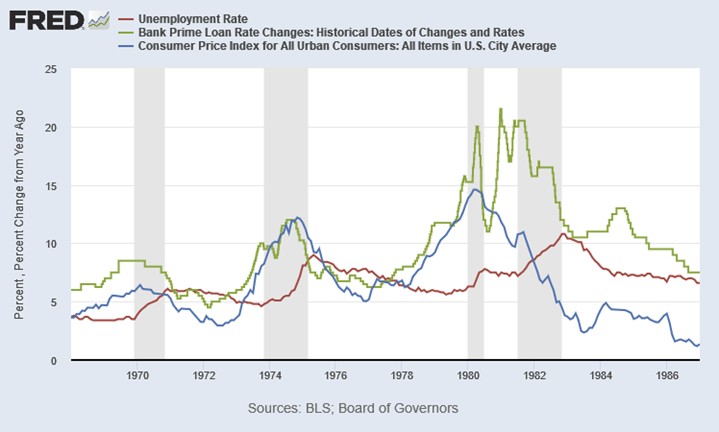

When mandatory wage and price controls came to a complete end in 1974, the aftermath was far from pleasant. Energy shortages and high food costs contributed to an increase in inflation and to recession, and the pressure that built up after the period of controls lead into the destructive double-digit inflation that plagued the early months of the Ford administration. Three years after controls had complete [sic] ended, both unemployment and inflation hovered around 7 percent, and there was even nostalgia for the “good old days” in 1971 when we had only 4 percent inflation and 6 percent unemployment.

–President Nixon, RN: The Memoirs of Richard Nixon

Unemployment hit 9% in May of 1975. Inflation reached double-digit in 1974 and 1979. The U.S. dollar price for a barrel of oil rose from $3.35 in January 1970 to $32.50 by the end of the 1970s. The U.S. consumer price index rose by 106 percent during the 1970s. The high interest-rate that followed brought on the recession in the early 1980s.

“The U.S. and other western countries struggled to cope with the inflationary shock. Corporate profitability suffered, encouraging firms to move their production plants to parts of the world where labour costs were cheaper. By the time the US started to take draconian steps to curb inflation at the end of the 1970s, Deng Xiaoping was launching the reforms that would turn China from an economic backwater into an industrial superpower. Fifty years after the collapse of the Bretton Woods system, China has emerged as a bigger threat to the US than the Soviet Union ever was”. (Elliott 2021)

The current official price for gold stock on Fed balance sheet is at $42.22 per ounce (as of October, 2022, source https://www.federalreserve.gov/data/intlsumm/current.htm). By the end of the 1970s, gold had risen 1200% to more than $455. The open market price in 2022 is between $2091 and $1621 (as of November 25, 2022).

THE CANTILLON EFFECT

Income inequality has significantly increased since the late 1960s, coinciding with the onset of the great inflation and welfare expansion. Since the Nixon presidency, richest Americans has experienced the fastest income growth while the real household income stagnated.

One often-downplayed consequence of monetary expansion is recognized by Irish economist Charles Cantillon (1680-1734). Cantillon observed that when money supply expands, those closest to the source of new money benefits the most, because they can purchase assets before the inflation occur. Those farthermost from the source of new money suffer the most, because they will bear the burden of inflation before their wages catch up with the price increase.

In other words, when massive amount of new money is created, not only does it lead to inflation but also chooses winners and losers. In our modern economy, the money expansion by central banks favors government, large corporations (that lobby the congress), and investors of these corporations. The accumulated effect leads to Plutocracy (government by the wealthy, of the wealthy, and for the wealthy) and Plutonomy (concentration of wealth), and threatens democracy. This effect is demonstrated by the stagnant real median household income over the past decades while asset price soared with the cost of living. When politicians advocate the “multiplier effect” of loose monetary policy “for the poor,” they conveniently leave out the fact that such policy exacerbates income inequality and worsens economic conditions for savers, people on fixed incomes, and wage earners, whose income increase persistently fall behind the inflation.

Consider the following recent headlines that demonstrate the Cantillon Effect in action, and how it bestows power and spreads corruption through central bankers, government insiders, and investment firms:

IS THIS TIME DIFFERENT?

There are two leading causes of inflation we’re seeing today. The first cause of inflation is a once-in-a-century pandemic. Not only did it shut down our global economy, it threw the supply chain and demand completely out of whack…

And this year we have a second cause — a second cause: Mr. Putin’s war in Ukraine.

You saw — we saw in March that 60 percent of inflation that month was due to price increases at the pump for gasoline.

Putin’s war has raised food prices as well, because Ukraine and Russia are two of the world’s major breadbaskets of — for wheat and corn — …Normally — normally, we’d have already begun to export them into the market. … But it’s difficult because, again, of Putin and the Russian invasion of Ukraine.

– President Joe Biden, May 10, 2022

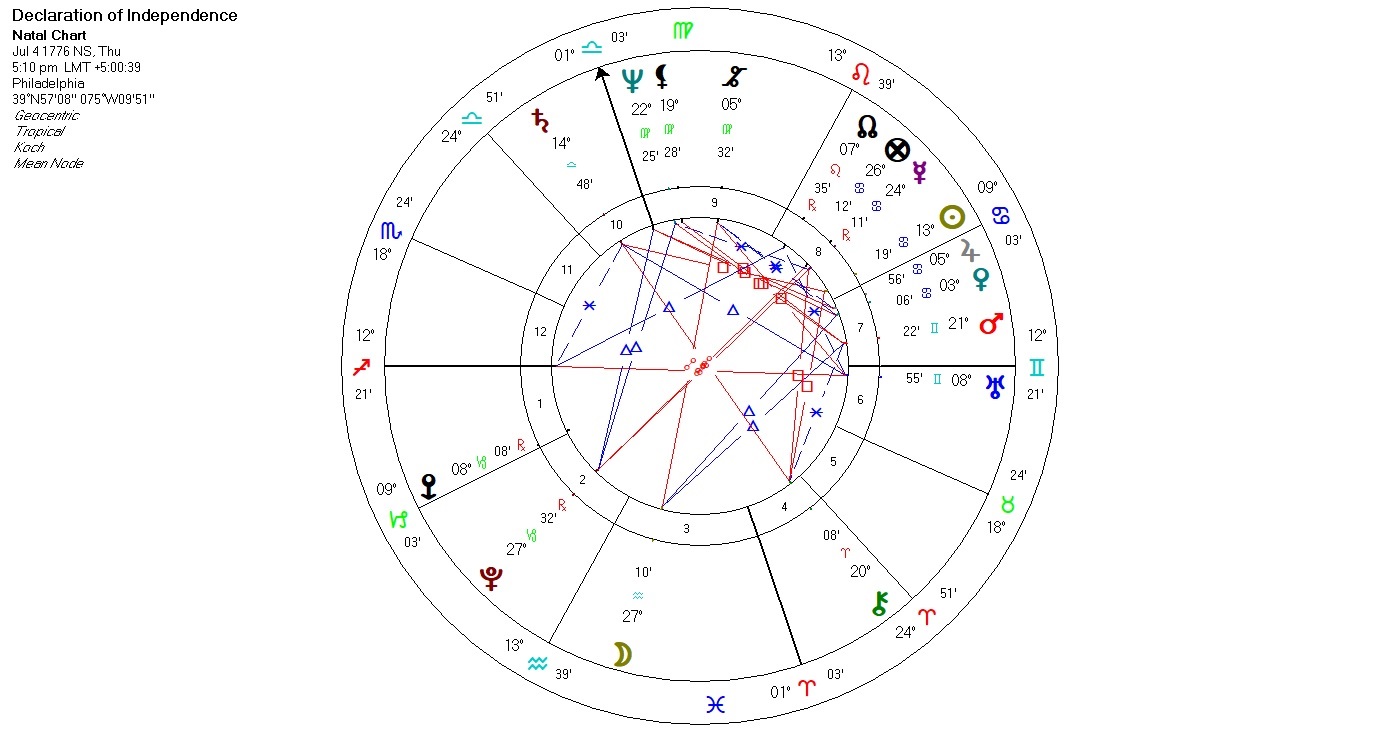

At the time of writing, the third and final conjunction of U.S. Pluto return is fast approaching. The difference between a Pluto trine in the 1970s and current Pluto return is that this time around, the transiting Pluto is both working for and against the U.S. The outward destruction and inner transformation –both constructive and destructive –work as one. The corruption (Pluto) in value (2nd house) is more intensified; so is the downfall and resurrection.

Pluto energy is both intensifying and transformative. Collectively, this energy rarely acts under freewill. What we’re presently witnessing (as of December 2022) is a strong and self-destructive force that will not quit until both fundamental change and significant collateral damage occur.

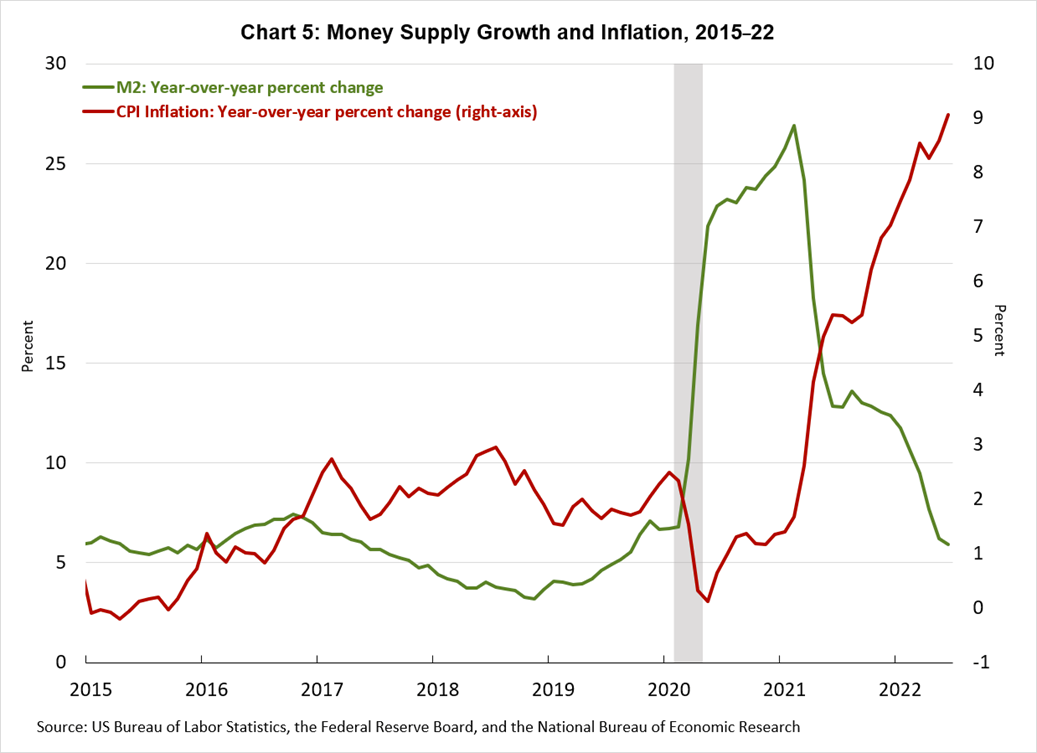

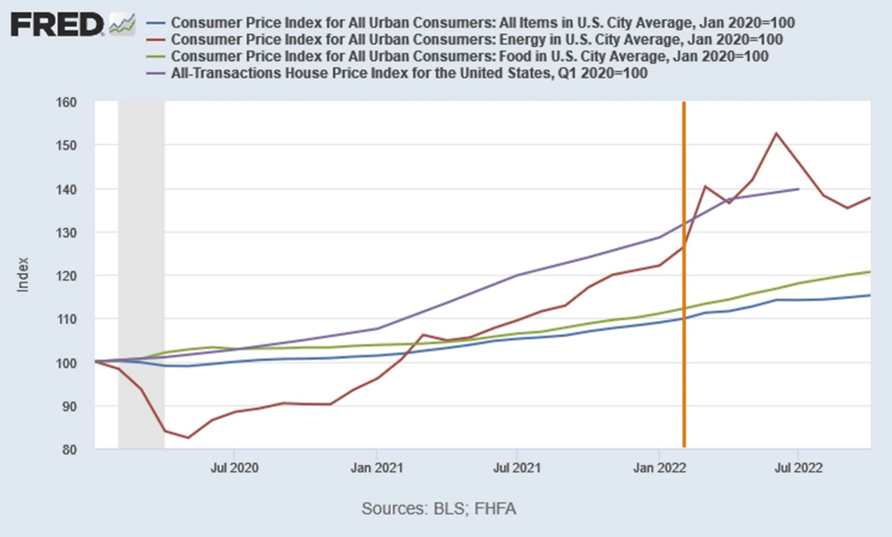

U.S.’s second house Pluto historically triggers money, currency and trade issue during important transits, this time is no different. Economists and market observers have come to the realization that the inflation/stagflation is resurfacing. This time, the Fed, caught between high inflation and high interest rate, is out of arsenals. “If the Fed runs down the SOMA (System Open Market Account. Fed’s asset portfolio containing the assets acquired and to be sold during open market operations) portfolio too much, they will break something in the market. If they don’t, we are stuck with inflation.” (Chavez-Dreyfuss 2022). Currently, the National debt to GDP ratio is at the highest since World War II. The debt servicing cost is at a steady up trend, and the treasury market liquidity is at crisis-level low.

Reminiscent of the great inflation of the 1970s, we are facing social and geopolitical tensions, overreaching government, volatile financial markets, and high inflation. In addition, we have unsustainable level of government and private debt, and a formidable geopolitical opponent to whom we continue to transfer funding, data, and advanced technology. In Nixon’s words: “the most formidable enemy that has ever existed in the history of the world” –China.

We won’t know to what extent and how this Pluto Return will manifest until the dust settles. If history is any guide, the inflation will not be transitory and the recession will not be shallow. Whatever temporary fix for structural problems will have long-lasting impact and unintended consequences.

It would be prudent to review major legislation and executive orders during the crucial Pluto return period (between March 2021 to December 2023). The policies that aim to solve long-term problems with political compromises –or worse, outright corruption –will not work as intended, and will likely carry pernicious consequences. It’s not too late to recognize the folly of our experts and officials, and the destruction the political class can inflict on our lives. The least we can do is to insulate ourselves as much as possible in the wake of their short-sighted and disastrous policies.

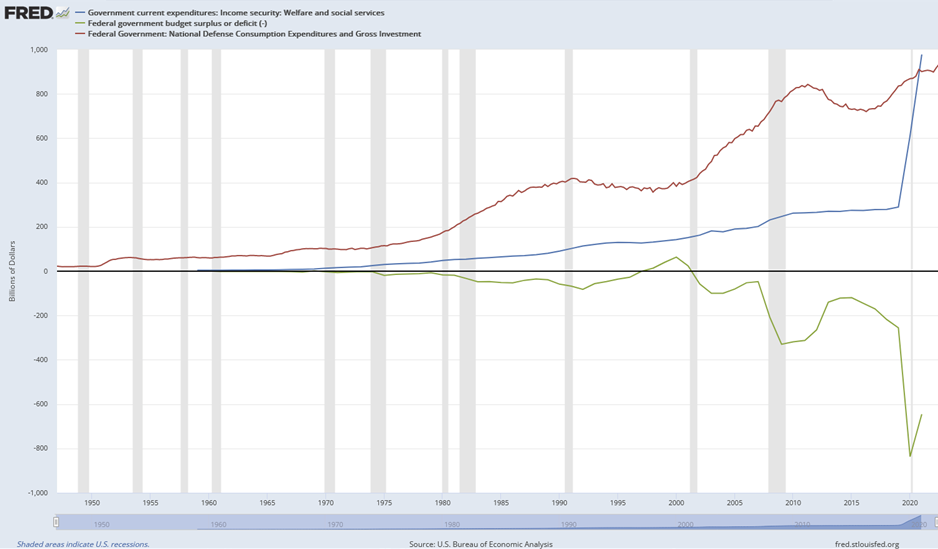

Government current expenditures: Welfare and social services (Blue)

Federal Government: National Defense Consumption: Expenditures and Gross Investment (Red)

Conservatives are always at a disadvantage when speaking about economics because their belief that some pain may be necessary now to save the patient later is conventionally interpreted by liberal politicians and commentators as “heartlessness” or “callous indifference to human suffering.”

It is unfortunate that the politics of economics has come to dictate action more than the economics of economics. Not surprisingly, when prudence clashes with political reality, the latter sometimes triumphs.

—President Richard Nixon, RN: The Memoirs of Richard Nixon

ADDITIONAL READING

- Turmoil in the Second House – The U.S. Pluto Return (2021-2023) Part 1: Astrology

- Turmoil in the Second House – The U.S. Pluto Return (2021-2023) Part 2: Born on the Battlefront

- Turmoil in the Second House – The U.S. Pluto Return (2021-2023) Part 3: History Rhymes (1) |Panic of 1819 and The Missouri Compromise (1819-1821)

- Turmoil in the Second House – The U.S. Pluto Return (2021-2023) Part 3: History Rhymes (2) | The Nixon Shock

REFERENCE

Abrams, Burton A. 2006. “How Richard Nixon Pressured Arthur Burns: Evidence from the Nixon Tapes.” Journal of Economic Perspectives, no. Volume 20, Number 4: 177–88. https://fraser.stlouisfed.org/title/journal-economic-perspectives-1167/richard-nixon-pressured-arthur-burns-evidence-nixon-tapes-2388.

Bordo, Michael D. 2018. “The Imbalances of the Bretton Woods System 1965 to 1973: U.S. Inflation, The Elephant in the Room.” NBER. National Bureau of Economic Research. December 2018. http://www.nber.org/papers/w25409.

Bordo, Michael, Eric Monnet, and Alain Naef. 2017. “The Gold Pool (1961-1968) and the Fall of the Bretton Woods System. Lessons for Central Bank Cooperation.” National Bureau of Economic Research. 2017. https://economics.ucdavis.edu/events/papers/copy2_of_417Bordo.pdf.

Bryan, Michael. 2013. “The Great Inflation .” Federal Reserve History. November 22, 2013. https://www.federalreservehistory.org/essays/great-inflation.

Butkiewicz, James L., and Scott Ohlmacher. 2021. “Ending Bretton Woods – The Economic Historian.” The Economic Historian. December 7, 2021. https://economic-historian.com/2021/12/ending-bretton-woods/.

Chavez-Dreyfuss, Gertrude. 2022. “Analysis: Nagging U.S. Treasury Liquidity Problems Raise Fed Balance Sheet Predicament.” Reuters. November 8, 2022. https://www.reuters.com/markets/us/nagging-us-treasury-liquidity-problems-raise-fed-balance-sheet-predicament-2022-11-08/.

Eichengreen, Barry. 2000. “From Benign Neglect to Malignant Preoccupation: U.S. Balance-of-Payments Policy in the 1960s.” National Bureau of Economic Research, March.

Elliott, Larry. 2021. “Rise of Cryptocurrencies Can Be Traced to Nixon Abandoning Gold in 1971.” The Guardian. August 15, 2021. https://www.theguardian.com/business/2021/aug/15/rise-of-cryptocurrencies-can-be-traced-to-nixon-abandoning-gold-in-1971.

Ferrell, Robert H. 2010. Inside the Nixon Administration: The Secret Diary of Arthur Burns, 1969-1974. University Press of Kansas.

Ghizoni, Sandra Kollen. 2013. “Nixon Ends Convertibility of U.S. Dollars to Gold and Announces Wage/Price Controls.” Federal Reserve History. November 2013. https://www.federalreservehistory.org/essays/gold-convertibility-ends.

Ghosh, Atish Rex. 2021. “From the History Books: The Rethinking of the International Monetary System.” IMF Blog. August 16, 2021. https://www.imf.org/en/Blogs/Articles/2021/08/16/from-the-history-books-the-rethinking-of-the-international-monetary-system.

Ghosh, AtishRex. 2021. “Behind Closed Doors.” International Monetary Fund|Finance & Development. September 2021. https://www.imf.org/en/Publications/fandd/issues/2021/09/book-review-three-days-at-camp-david-garten.

Hammes, David, and Douglas Wills. 2005. “Black Gold: The End of Bretton Woods and the Oil-Price Shocks of the 1970s.” The Independent Review.

Hetzel, Robert L. 2013. “Launch of the Bretton Woods System.” Federal Reserve History. November 22, 2013. https://www.federalreservehistory.org/essays/bretton-woods-launched.

Humpage, Owen. 2013. “The Smithsonian Agreement.” Federal Reserve History. November 22, 2013. https://www.federalreservehistory.org/essays/smithsonian-agreement.

Lehrman, Lewis E. 2011. “The Nixon Shock Heard ’Round the World.” The Wall Street Journal. August 15, 2011. https://www.wsj.com/articles/SB10001424053111904007304576494073418802358.

Lowenstein, Roger. 2011. “The Nixon Shock.” Bloomberg Businessweek. August 4, 2011. https://www.bloomberg.com/news/articles/2011-08-04/the-nixon-shock.

The Washington Post. 2019. “How Paul Volcker Beat Inflation and Saved an Independent Fed.” Washington Post. December 10, 2019. https://www.washingtonpost.com/business/economy/how-paul-volcker-beat-inflation-and-saved-an-independent-fed/2019/12/10/7e58d7ae-1b64-11ea-87f7-f2e91143c60d_story.html.

Mandelman, Federico, and Brent Meyer. 2022. “Lessons from the Past: Can the 1970s Help Inform the Future Path of Monetary Policy?” Federal Reserve Bank of Atlanta. August 31, 2022. https://www.atlantafed.org/blogs/macroblog/2022/08/31/can-1970s-help-inform-future-path-of-monetary-policy.aspx.

Manly, Ronan. 2021. “British Requests for $3 Billion in US Treasury Gold – The Trigger That Closed the Gold Window.” BullionStar. August 16, 2021. https://www.bullionstar.com/blogs/ronan-manly/british-requests-for-3-billion-in-us-treasury-gold-the-trigger-that-closed-the-gold-window/.

Meltzer, Allan H. 2005. “Origins of the Great Inflation.” Federal Reserve Bank of St. Louis Review, March 2005.

“Milestones: 1969–1976 – Nixon and the End of the Bretton Woods System, 1971–1973.” n.d. Office of the Historian. Accessed November 15, 2022. https://history.state.gov/milestones/1969-1976/nixon-shock.

“Money: De Gaulle v. the Dollar.” 1965. Time, February 1965.

“Money Matters: An IMF Exhibit — The Importance of Global Cooperation | System in Crisis (1959-1971).” n.d. International Monetary Fund. https://www.imf.org/external/np/exr/center/mm/eng/sc_sub_3.htm.

New York Times. 1971. “Call to Economic Revival,” August 16, 1971.

Nichter, Luke. 2015. Richard Nixon and Europe. Cambridge University Press.

Nixon, Richard Milhous. 1978. RN: The Memoirs of Richard Nixon. Touchstone Books.

Nixon Tapes, Oval Office 570-44. 1971. 12:07-12:53 pm

Ohlmacher, Scott W. 2009. “Ths Dissolution of the Bretton Woods System, Evience from the Nixon Tapes, August-December 1971.” Honors Degree Thesis, University of Delaware.

Rand, Ayn. 1967. Capitalism. Signet. Gold and Economic Freedom by Alan Greenspan

Rothbard, Murray N. 2018. “The Monetary Breakdown of the West.” Mises Institute. March 7, 2018. https://mises.org/library/monetary-breakdown-west.

Strong, Bill, John Hathaway, and Stephanie Pomboy. 2021. “ ‘Nixon Shock’ 50 Years Later, Remembering the 1970s.” Sprott Insights. August 15, 2021. https://sprott.com/insights/video-nixon-shock-50-years-later-remembering-the-1970s.

“The Challenge of Peace: President Nixon’s New Economic Policy.” 2014. Richard Nixon Foundation. August 15, 2014. https://www.nixonfoundation.org/2014/08/challenge-peace-nixons-new-economic-policy/.

“U.S. Spent $141‐Billion In Vietnam in 14 Years.” 1975. The New York Times. May 1, 1975. https://www.nytimes.com/1975/05/01/archives/us-spent-141billion-in-vietnam-in-14-years.html.

Wapshott, Nicholas. 2021. Samuelson Friedman: The Battle Over the Free Market. W. W. Norton & Company.

Yergin, Daniel, and Joseph Stanislaw. 1997. The Commanding Heights.

©2022 Brave New Real. All rights reserved.